Filed Pursuant to Rule 424(b)(5)

Registration No. 333-229118

PROSPECTUS SUPPLEMENT

(To Prospectus Dated February 4, 2019)

Up to $20,000,000

Common Stock

We have entered into an Open Market Sale AgreementSM, or sales agreement, with Jefferies LLC, or Jefferies, dated December 13, 2019, relating to shares of our common stock, $0.0001 par value per share, offered by this prospectus supplement and the accompanying prospectus. In accordance with the terms of the sales agreement, we may offer and sell shares of our common stock having an aggregate offering price of up to $20,000,000 from time to time through Jefferies acting as sales agent, at our discretion.

Our common stock is listed on The Nasdaq Capital Market under the symbol “AVCO.” On December 12, 2019, the closing sale price of our common stock on The Nasdaq Capital Market was $2.32 per share.

Upon our delivery of a placement notice and subject to the terms and conditions of the sales agreement, Jefferies may sell shares of our common stock by methods deemed to be an “at the market offering” as defined in Rule 415(a)(4) promulgated under the Securities Act of 1933, as amended, or the Securities Act.. Jefferies will act as sales agent using its commercially reasonable efforts consistent with its normal trading and sales practices, on mutually agreed terms between Jefferies and us. There is no arrangement for funds to be received in any escrow, trust or similar arrangement.

Jefferies will be entitled to compensation at a fixed commission rate of 3.0% of the gross proceeds of each sale of shares of our common stock. See “Plan of Distribution” beginning on page S-6 for additional information regarding the compensation to be paid to Jefferies. In connection with the sale of our common stock on our behalf, Jefferies will be deemed to be an “underwriter” within the meaning of the Securities Act and the compensation of Jefferies will be deemed to be underwriting commissions or discounts. We have also agreed to provide indemnification and contribution to Jefferies with respect to certain liabilities, including liabilities under the Securities Act.

Investing in our securities involves a high degree of risk. Before making an investment decision, please read the information under the heading “Risk Factors” beginning on page S-3 of this prospectus supplement and in the documents incorporated by reference into this prospectus supplement and the accompanying prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus supplement or the accompanying prospectus. Any representation to the contrary is a criminal offense.

Jefferies

December 13, 2019

TABLE OF CONTENTS

| PROSPECTUS SUPPLEMENT | |

| Page | |

| About This Prospectus Supplement | S-ii |

| Cautionary Note Regarding Forward-Looking Statements | S-iii |

| Prospectus Supplement Summary | S-1 |

| Risk Factors | S-3 |

| Use of Proceeds | S-4 |

| Dilution | S-5 |

| Plan of Distribution | S-6 |

| Legal Matters | S-7 |

| Experts | S-7 |

| Where You Can Find More Information | S-7 |

| Incorporation by Reference | S-7 |

| ACCOMPANYING PROSPECTUS | |

| Page | |

| About This Prospectus | 1 |

| About the Company | 2 |

| Recent Development | 18 |

| Risk Factors | 21 |

| Cautionary Note Regarding the Forward-Looking Statements | 49 |

| Use of Proceeds | 50 |

| Dividend Policy | 50 |

| Offering and Listing Details | 50 |

| Description of Capital Stock | 51 |

| Description of Warrants | 52 |

| Description of Units | 53 |

| Income Tax Considerations | 53 |

| Plan of Distribution | 54 |

| Where You Can Find More Information | 55 |

| Incorporation by Reference | 55 |

| Material Changes | 56 |

| Legal Matters | 57 |

| Experts | 57 |

S-i

ABOUT THIS PROSPECTUS SUPPLEMENT

This prospectus supplement and the accompanying prospectus relate to the offering of our common stock. Before buying any of the common stock that we are offering, we urge you to carefully read this prospectus supplement and the accompanying prospectus, together with the information incorporated by reference as described under the heading “Incorporation by Reference” in this prospectus supplement and the accompanying prospectus. These documents contain important information that you should consider when making your investment decision.

This document is in two parts. The first part is this prospectus supplement, which describes the specific terms of this offering and also adds to and updates information contained in the accompanying prospectus and the documents incorporated by reference herein or therein. The second part, the accompanying prospectus, provides more general information. Generally, when we refer to this prospectus, we are referring to both parts of this document combined. To the extent there is a conflict between the information contained in this prospectus supplement and the information contained in the accompanying prospectus or any document incorporated by reference herein or therein filed prior to the date of this prospectus supplement, you should rely on the information in this prospectus supplement; provided that if any statement in one of these documents is inconsistent with a statement in another document having a later date—for example, a document incorporated by reference in the accompanying prospectus—the statement in the document having the later date modifies or supersedes the earlier statement.

We further note that the representations, warranties and covenants made by us in any agreement that is filed as an exhibit to any document that is incorporated by reference herein or in the accompanying prospectus were made solely for the benefit of the parties to such agreement, including, in some cases, for the purpose of allocating risk among the parties to such agreement, and should not be deemed to be a representation, warranty or covenant to you. Moreover, such representations, warranties or covenants were accurate only as of the date when made. Accordingly, such representations, warranties and covenants should not be relied on as accurately representing the current state of our affairs.

You should rely only on the information contained in, or incorporated by reference in, this prospectus supplement, the accompanying prospectus and in any free writing prospectus that we may authorize for use in connection with this offering. We have not, and Jefferies has not, authorized anyone to provide you with any information other than that contained or incorporated by reference in this prospectus supplement, in the accompanying prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We and Jefferies take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are not, and Jefferies is not, making an offer to sell, or soliciting an offer to purchase, the securities offered by this prospectus supplement and the accompanying prospectus in any jurisdiction to or from any person to whom or from whom it is unlawful to make such offer or solicitation of an offer in such jurisdiction. The information contained in this prospectus supplement, the accompanying prospectus, the documents incorporated by reference herein or therein, and in any free writing prospectus prepared by or on behalf of us that we may authorize for use in connection with this offering is accurate only as of the date of those respective documents. Our business, financial condition, results of operations and prospects may have changed since those dates. It is important for you to read and consider all information contained in this prospectus supplement, the accompanying prospectus, the documents incorporated by reference herein and therein, and any free writing prospectus prepared by or on behalf of us that we may authorize for use in connection with this offering, in their entirety, before making an investment decision. You should also read and consider the information in the documents to which we have referred you in the sections entitled “Where You Can Find More Information” and “Incorporation by Reference” in this prospectus supplement and the accompanying prospectus.

We and Jefferies are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The distribution of this prospectus supplement and the accompanying prospectus and the offering of the common stock in certain jurisdictions may be restricted by law. Persons outside the United States who come into possession of this prospectus supplement and the accompanying prospectus must inform themselves about, and observe any restrictions relating to, the offering of the common stock and the distribution of this prospectus supplement and the accompanying prospectus outside the United States. This prospectus supplement and the accompanying prospectus do not constitute, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy, any securities offered by this prospectus supplement and the accompanying prospectus by any person in any jurisdiction in which it is unlawful for such person to make such an offer or solicitation.

Unless otherwise stated, all references in this prospectus supplement and the accompanying prospectus to “we”, “us”, “our”, “Company”, “our company”, “Avalon GloboCare” and “Avalon” refer to Avalon GloboCare Corp., a Delaware corporation, either alone or together with our consolidated subsidiaries as the context requires.

This prospectus supplement and the accompanying prospectus contains references to our trademarks and to trademarks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus supplement and the accompanying prospectus, including logos, artwork and other visual displays, may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend our use or display of other companies’ trade names or trademarks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

S-ii

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus supplement and the accompanying prospectus contain, and the documents incorporated by reference herein and therein and any free writing prospectus that we have authorized for use in connection with this offering may contain, forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements other than statements of historical facts contained in this prospectus supplement, the accompanying prospectus and the information we incorporate by reference are forward-looking statements. These statements relate to future events or to our future operating or financial performance and involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. Forward-looking statements may include, but are not limited to statements about:

| ● | our ability to attract and retain management; |

| ● | our ability to raise capital when needed and on acceptable terms and conditions; |

| ● | the intensity of competition; |

| ● | general economic conditions; |

| ● | changes in regulations; |

| ● | whether the market for healthcare services continues to grow, and, if it does, the pace at which it may grow; and |

| ● | our ability to compete against large competitors in a rapidly changing market. |

In some cases, you can identify forward-looking statements by terms such “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “project,” “target,” “will” and other words and terms of similar meaning. These statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward-looking statements. We discuss many of these risks in greater detail under the heading “Risk Factors” in this prospectus supplement and in our SEC filings.

You should read this prospectus supplement, the accompanying prospectus, the documents we have filed with the SEC that are incorporated by reference and any free writing prospectus that we have authorized for use in connection with this offering completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of the forward-looking statements in the foregoing documents by these cautionary statements. You should not place undue reliance on these statements. Forward-looking statements speak only as of the date of the document containing the applicable statement. We do not undertake any obligation to publicly update any forward-looking statements.

S-iii

This summary highlights certain information about us, this offering and selected information contained elsewhere in or incorporated by reference in this prospectus supplement. This summary is not complete and does not contain all of the information that you should consider before deciding whether to invest in our securities. For a more complete understanding of our company and this offering, we encourage you to read and consider carefully the more detailed information in this prospectus supplement and the accompanying prospectus, including the information included under the heading “Risk Factors” in this prospectus supplement beginning on page S-3, the information included under the heading “Risk Factors” in the accompanying prospectus beginning on page 21, the information incorporated by reference in this prospectus supplement and the accompanying prospectus, which is described under “Where You Can Find More Information” and “Incorporation by Reference,” and the information included in any free writing prospectus that we have authorized for use in connection with this offering.

Overview

We are a clinical-stage, leading CellTech bio-developer dedicated to advancing and empowering innovative, transformative immune effector cell therapy and exosome technology. We also provide strategic advisory and outsourcing services to facilitate and enhance our clients’ growth, development, as well as competitiveness in healthcare and CellTech industry markets.

Our subsidiary and joint venture structure contribute to investor flexibility and research and development focus, enabling us to establish our leading role in the fields of immune effector cell therapy (including CAR-T and CAR-NK), exosome-based regenerative therapeutics (our Avalon Clinical-grade Tissue-specific Exosome, or ACTEXTM, platform), as well as “liquid biopsy” diagnostics.

We achieve and foster seamless integration of unique verticals to bridge and accelerate innovative research, bio-process development, clinical programs and product commercialization.

Our upstream innovative research includes:

| ● | Co-development of ACTEXTM with Weill Cornell Medicine; |

| ● | Novel therapeutic and diagnostic targets development utilizing QTY-code protein design technology with Massachusetts Institute of Technology, orMIT; and |

| ● | Co-development of next generation, transposon-based, multi-target CAR-T, CAR-NK and other immune effector cell therapeutic modalities with Arbele Corp. |

Our midstream bio-processing and bio-production facility is located in Nanjing, China with state-of-the-art, automated GMP and QC/QA infrastructure for standardized bio-manufacturing of clinical-grade cellular products involved in our clinical programs in immune effector cell therapy, regenerative therapeutics, as well as bio-banking.

Our downstream medical team and facility consists of top-rated affiliated hospital network and experts specialized in hematology, oncology, cellular immunotherapy, hematopoietic stem/progenitor cell transplant, as well as regenerative therapeutics. Our major clinical programs include:

| ● | AVA-001: We have initiated our first-in-human clinical trial of our CD19 CAR-T candidate, AVA-001, in August 2019 at the Hebei Yanda Lu Daopei Hospital and Beijing Lu Daopei Hospital in China for the indication of relapsed/refractory B-cell acute lymphoblastic leukemia and non-Hodgkin Lymphoma. AVA-001 is characterized by the utilization of 4-1BB (CD137) co-stimulatory signaling pathway, conferring a strong anti-cancer activity during pre-clinical study. It also features a shorter bio-manufacturing time which leads to advantage of prompt treatment to patients with these dreadful hematologic malignancies. We plan to recruit 20 patients (under registered clinical trial NCT03952523) for safety and efficacy studies. |

| ● | AVA-101: Our transposon-based, multi-targeted CAR-T candidate, AVA-101 (co-developed with Arbele Corp.), has entered the pre-clinical process development and validation phase. AVA-101 features non-viral, transposon-engineered CAR-T with multiple anti-cancer targets, as well as possessing molecular safety-switch mechanism to minimize the side effects, such as cytokine release syndrome and neurotoxicity, often associated with conventional CAR-T cellular therapy. We anticipate this next generation of potentially more effective and safer CAR-T candidate will proceed to a first-in-human clinical study in the later part of 2020. |

| ● | AVA-202: We have recently completed the standardized bio-production process of tissue-specific, clinical-grade exosomes, a co-development endeavor with Weill Cornell Medicine with focus on angiogenic exosomes derived from endothelial cells which promote blood vessel formation and wound healing. We are further developing this technology platform into a therapeutic candidate, AVA-202, and plan to initiate international multi-centered clinical studies in unmet medical areas of vascular diseases and wound healing, including treatment of diabetic foot ulcer. |

The commercialization phase of our ACTEXTM-based product development is underway to enter the markets of skin care, scar removal, and hair growth through in-house development and strategic partnership.

Company Information

We were incorporated under the laws of the State of Delaware on July 28, 2014 under the name Global Technologies Corp. On October 18, 2016, we changed our name to Avalon GloboCare Corp. Our principal executive offices are located at 4400 Route 9 South, Suite 3100, Freehold, New Jersey 07728, and our telephone number is (732) 780-4400. Our Internet website is www.avalon-globocare.com. The information on, or that can be accessed through, our website is not part of this prospectus supplement, and you should not rely on any such information in making the decision whether to purchase our securities.

S-1

The Offering

| Common stock offered by us | Shares of our common stock having an aggregate offering price of up to $20,000,000. |

| Common stock to be outstanding after this offering | Up to 8,620,690 shares, assuming sales at a price of $2.32 per share, which was the closing price of our common stock on The Nasdaq Capital Market on December 12, 2019. The actual number of shares issued will vary depending on the sales price under this offering. |

| Plan of Distribution | “At the market offering” that may be made from time to time through our agent, Jefferies LLC. See the section entitled “Plan of Distribution” on page S-6 of this prospectus supplement. |

| Use of Proceeds | We currently intend to use the net proceeds from this offering to fund our core technology platform development and clinical studies in exosome-based liquid biopsy and regenerative therapeutics, next-generation multi-targeted CAR-T immunotherapy, co-development projects with MIT and Weill Cornell, as well as for working capital and other general corporate purposes. See the section entitled “Use of Proceeds” on page S-4 of this prospectus supplement. |

| Risk Factors | This investment involves a high degree of risk. See “Risk Factors” beginning on page S-3 of this prospectus supplement and the other information included in, or incorporated by reference into, this prospectus supplement for a discussion of certain factors you should carefully consider before deciding to invest in shares of our common stock. |

| Nasdaq Capital Market symbol | AVCO |

The number of shares of our common stock to be outstanding after this offering is based on 75,771,056 shares of our common stock issued and outstanding as of September 30, 2019 and excludes:

| ● | 5,070,000 shares of common stock issuable upon exercise of outstanding stock options at a weighted-average exercise price of $1.43 per share as of September 30, 2019; and |

| ● | 1,714,288 shares of common stock issuable upon exercise of outstanding warrants to purchase common stock at a weighted-average exercise price of $3.50 per share as of September 30, 2019. |

S-2

An investment in our securities involves a high degree of risk. Before deciding whether to invest in our securities, you should consider carefully the risks described below and discussed under the sections captioned “Risk Factors” contained in our Annual Report on Form 10-K for the year ended December 31, 2018 and our Quarterly Report on Form 10-Q for the quarter ended September 30, 2019, which are incorporated by reference in this prospectus supplement and the accompanying prospectus, together with other information in this prospectus supplement, the accompanying prospectus, the information and documents incorporated by reference, and in any free writing prospectus that we have authorized for use in connection with this offering. See “Where You Can Find More Information” and “Incorporation by Reference.” If any of these risks actually occurs, our business, financial condition, results of operations or cash flow could be harmed. This could cause the trading price of our common stock to decline, resulting in a loss of all or part of your investment. The risks described below and in the documents referenced above are not the only ones that we face. Additional risks not presently known to us or that we currently deem immaterial may also affect our business.

Risks Related To This Offering

If you purchase shares of common stock in this offering, you will suffer immediate and substantial dilution of your investment.

The price per share of our common stock in this offering may exceed the net tangible book value per share of our common stock outstanding prior to this offering. Therefore, if you purchase shares of our common stock in this offering, you may pay a price per share that substantially exceeds our net tangible book value per share after this offering. To the extent shares are issued under outstanding options or warrants at exercise prices lower than the price of our common stock in this offering, you will incur further dilution. Assuming that an aggregate of 8,620,690 shares of our common stock are sold at a price of $2.32 per share, the last reported sale price of our common stock on The Nasdaq Capital Market on December 12, 2019, for aggregate proceeds to us of $20,000,000, and after deducting commissions and estimated aggregate offering expenses payable by us, you will experience immediate dilution of $2.03 per share, representing the difference between our as adjusted net tangible book value per share as of September 30, 2019 after giving effect to this offering and the assumed offering price. See the section entitled “Dilution” below for a more detailed illustration of the dilution you would incur if you participate in this offering.

You may experience future dilution as a result of future equity offerings.

In order to raise additional capital, we may in the future offer additional shares of our common stock or other securities convertible into or exchangeable for our common stock at prices that may not be the same as the price per share in this offering. We may sell shares or other securities in any other offering at a price per share that is less than the price per share paid by investors in this offering, and investors purchasing shares or other securities in the future could have rights superior to existing stockholders. The price per share at which we sell additional shares of our common stock, or securities convertible or exchangeable into common stock, in future transactions may be higher or lower than the price per share paid by investors in this offering.

An active trading market for our common stock may not be sustained.

Although our common stock is listed on The Nasdaq Capital Market, an active trading market for our shares may not be sustained. If an active market for our common stock does not continue, it may be difficult for you to sell shares you purchase in this offering without depressing the market price for the shares, or at all. An inactive trading market for our common stock may also impair our ability to raise capital to continue to fund our operations by selling shares and may impair our ability to acquire other companies or technologies by using our shares as consideration.

We have broad discretion in the use of our cash and cash equivalents, including the net proceeds we receive in this offering, and may not use them effectively.

Our management will have broad discretion in the application of the net proceeds we receive in this offering, including for any of the purposes described in the section entitled “Use of Proceeds,” and you will not have the opportunity as part of your investment decision to assess whether our management is using the net proceeds appropriately. Because of the number and variability of factors that will determine our use of our net proceeds from this offering, their ultimate use may vary substantially from their currently intended use. The failure by our management to apply these funds effectively could result in financial losses that could have a material adverse effect on our business and cause the price of our common stock to decline. Pending their use, we may invest our net proceeds from this offering in short-term, investment-grade, interest-bearing securities. These investments may not yield a favorable return to our stockholders.

S-3

We currently intend to use the net proceeds from this offering to fund our core technology platform development and clinical studies in exosome-based liquid biopsy and regenerative therapeutics, next-generation multi-targeted CAR-T immunotherapy, co-development projects with MIT and Weill Cornell, as well as for working capital and other general corporate purposes.

The expected use of net proceeds from this offering represents our intentions based upon our current plans and business conditions, which could change in the future as our plans and business conditions evolve. The amount and timing of these expenditures will depend on a number of factors, including the progress of our research and development efforts, the progress of any partnering efforts, technological advances and the competitive environment for our product candidates. Accordingly, you will be relying on the judgment of our management with regard to the use of these net proceeds, and you will not have the opportunity, as part of your investment decision, to assess whether the proceeds are being used appropriately. It is possible that the proceeds will be used in a way that does not yield a favorable, or any, return for us.

Pending application of the net proceeds as described above, we intend to invest the proceeds in investment grade interest bearing instruments, or will hold the proceeds in interest bearing or non-interest bearing bank accounts.

S-4

If you invest in this offering, your ownership interest will be diluted immediately to the extent of the difference between the public offering price per share and the as-adjusted net tangible book value per share of our common stock after giving effect to this offering. We calculate net tangible book value per share by dividing the net tangible book value, which is tangible assets less total liabilities, by the number of outstanding shares of our common stock. Dilution represents the difference between the portion of the amount per share paid by purchasers of shares in this offering and the as adjusted net tangible book value per share of our common stock immediately after giving effect to this offering. Our net tangible book value as of September 30, 2019 was approximately $5.7 million, or $0.08 per share.

After giving effect to the sale of our common stock pursuant to this prospectus supplement and accompanying prospectus in the aggregate amount of $20,000,000 at an assumed offering price of $2.32 per share, the last reported sale price of our common stock on The Nasdaq Capital Market on December 12, 2019, and after deducting commissions and estimated aggregate offering expenses payable by us, our net tangible book value as of September 30, 2019 would have been approximately $24.8 million, or $0.29 per share of common stock. This represents an immediate increase in the net tangible book value of $0.21 per share to our existing stockholders and an immediate dilution in net tangible book value of $2.03 per share to new investors. The following table illustrates this per share dilution:

| Assumed offering price per share | $ | 2.32 | ||||||

| Net tangible book value per share as of September 30, 2019 | $ | 0.08 | ||||||

| Increase per share attributable to new investors | $ | 0.21 | ||||||

| As-adjusted net tangible book value per share as of September 30, 2019 after giving effect to this offering | $ | 0.29 | ||||||

| Dilution per share to new investors purchasing shares in this offering | $ | 2.03 |

The table above assumes for illustrative purposes that an aggregate of 8,620,690 shares of our common stock are sold pursuant to this prospectus supplement and the accompanying prospectus at a price of $2.32 per share, the last reported sale price of our common stock on The Nasdaq Capital Market on December 12, 2019, for aggregate gross proceeds of $20,000,000. The shares sold in this offering, if any, will be sold from time to time at various prices. An increase of $1.00 per share in the price at which the shares are sold from the assumed offering price of $2.32 per share, assuming all of our common stock in the aggregate amount of $20,000,000 is sold at that price, would result in an adjusted net tangible book value per share after the offering of $0.30 per share and would increase the dilution in net tangible book value per share to new investors in this offering to $3.02 per share, after deducting commissions and estimated aggregate offering expenses payable by us. A decrease of $1.00 per share in the price at which the shares are sold from the assumed offering price of $2.32 per share, assuming all of our common stock in the aggregate amount of $20,000,000 is sold at that price, would result in an adjusted net tangible book value per share after the offering of $0.27 per share and would decrease the dilution in net tangible book value per share to new investors in this offering to $1.05 per share, after deducting commissions and estimated aggregate offering expenses payable by us. This information is supplied for illustrative purposes only.

The above discussion and table are based on 75,771,056 shares of our common stock issued and outstanding as of September 30, 2019 and excludes the following:

| ● | 5,070,000 shares of common stock issuable upon exercise of outstanding stock options at a weighted-average exercise price of $1.43 per share as of September 30, 2019; and |

| ● | 1,714,288 shares of common stock issuable upon exercise of outstanding warrants to purchase common stock at a weighted-average exercise price of $3.50 per share as of September 30, 2019. |

S-5

We have entered into a sales agreement with Jefferies, under which we may offer and sell up to $20.0 million of our shares of common stock from time to time through Jefferies acting as agent. Sales of our shares of common stock, if any, under this prospectus supplement and the accompanying prospectus will be made by any method that is deemed to be an “at the market offering” as defined in Rule 415(a)(4) under the Securities Act.

Each time we wish to issue and sell shares of common stock under the sales agreement, we will notify Jefferies of the number of shares to be issued, the dates on which such sales are anticipated to be made, any limitation on the number of shares to be sold in any one day and any minimum price below which sales may not be made. Once we have so instructed Jefferies, unless Jefferies declines to accept the terms of such notice, Jefferies has agreed to use its commercially reasonable efforts consistent with its normal trading and sales practices to sell such shares up to the amount specified on such terms. The obligations of Jefferies under the sales agreement to sell our shares of common stock are subject to a number of conditions that we must meet.

The settlement of sales of shares between us and Jefferies is generally anticipated to occur on the second trading day following the date on which the sale was made. Sales of our shares of common stock as contemplated in this prospectus supplement will be settled through the facilities of The Depository Trust Company or by such other means as we and Jefferies may agree upon. There is no arrangement for funds to be received in an escrow, trust or similar arrangement.

We will pay Jefferies a commission equal to 3.0% of the aggregate gross proceeds we receive from each sale of our shares of common stock. Because there is no minimum offering amount required as a condition to close this offering, the actual total public offering amount, commissions and proceeds to us, if any, are not determinable at this time. In addition, we have agreed to reimburse Jefferies for the fees and disbursements of its counsel, payable upon execution of the sales agreement, in an amount not to exceed $100,000. We estimate that the total expenses for the offering, excluding any commissions or expense reimbursement payable to Jefferies under the terms of the sales agreement, will be approximately $200,000. The remaining sale proceeds, after deducting any other transaction fees, will equal our net proceeds from the sale of such shares.

Jefferies will provide written confirmation to us before the open on The Nasdaq Capital Market on the day following each day on which shares of common stock are sold under the sales agreement. Each confirmation will include the number of shares sold on that day, the aggregate gross proceeds of such sales and the proceeds to us.

In connection with the sale of the shares of common stock on our behalf, Jefferies will be deemed to be an “underwriter” within the meaning of the Securities Act, and the compensation of Jefferies will be deemed to be underwriting commissions or discounts. We have agreed to indemnify Jefferies against certain civil liabilities, including liabilities under the Securities Act. We have also agreed to contribute to payments Jefferies may be required to make in respect of such liabilities.

The offering of our shares of common stock pursuant to the sales agreement will terminate upon the earlier of (i) the sale of all shares of common stock subject to the sales agreement and (ii) the termination of the sales agreement as permitted therein. We and Jefferies may each terminate the sales agreement at any time upon ten days’ prior notice.

This summary of the material provisions of the sales agreement does not purport to be a complete statement of its terms and conditions. A copy of the sales agreement will be filed as an exhibit to a current report on Form 8-K filed under the Exchange Act, and incorporated by reference in this prospectus supplement.

Jefferies and its affiliates may in the future provide various investment banking, commercial banking, financial advisory and other financial services for us and our affiliates, for which services they may in the future receive customary fees. In the course of its business, Jefferies may actively trade our securities for its own account or for the accounts of customers, and, accordingly, Jefferies may at any time hold long or short positions in such securities.

A prospectus supplement and the accompanying prospectus in electronic format may be made available on a website maintained by Jefferies, and Jefferies may distribute the prospectus supplement and the accompanying prospectus electronically.

S-6

The validity of the shares of common stock offered hereby will be passed upon for us by Goodwin Procter LLP, New York, New York. Jefferies LLC is being represented in connection with this offering by Cooley LLP, New York, New York.

RBSM LLP, an independent registered public accounting firm, has audited our consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2018, as set forth in their report dated March 26, 2019 (which contains an explanatory paragraph about our ability to continue as a going concern), which is incorporated by reference in this prospectus supplement and elsewhere in the registration statement to which this prospectus supplement relates. Our consolidated financial statements are incorporated by reference in reliance on RBSM LLP’s report, given on their authority as experts in accounting and auditing.

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly and current reports, proxy statements and other information with the SEC. Our SEC filings are available to the public over the Internet at the SEC’s website at www.sec.gov. Copies of certain information filed by us with the SEC are also available on our website at www.avalon-globocare.com. Our website is not a part of this prospectus supplement and is not incorporated by reference in this prospectus supplement.

This prospectus supplement is part of a registration statement that we filed with the SEC. The registration statement contains more information than this prospectus supplement and the accompanying prospectus regarding us and the securities, including certain exhibits and schedules. You can obtain a copy of the registration statement from the SEC’s website.

The SEC allows us to incorporate by reference in this prospectus supplement and the accompanying prospectus much of the information we file with the SEC, which means that we can disclose important information to you by referring you to those publicly available documents. The information that we incorporate by reference in this prospectus supplement and the accompanying prospectus is considered to be part of this prospectus supplement and the accompanying prospectus. Because we are incorporating by reference future filings with the SEC, this prospectus supplement and the accompanying prospectus is continually updated and those future filings may modify or supersede some of the information included or incorporated in this prospectus supplement and the accompanying prospectus. This means that you must look at all of the SEC filings that we incorporate by reference to determine if any of the statements in this prospectus supplement, the accompanying prospectus or in any document previously incorporated by reference have been modified or superseded. This prospectus supplement and the accompanying prospectus incorporate by reference the documents listed below (File No. 001-38728) and any future filings we make with the SEC under Sections 13(a), 13(c), 14 or 15(d) of the Exchange Act (in each case, other than those documents or the portions of those documents not deemed to be filed) until the offering of the securities under the registration statement is terminated or completed:

| ● | Annual Report on Form 10-K for the fiscal year ended December 31, 2018, filed on March 26, 2019; |

| ● | Quarterly Reports on Form 10-Q for the fiscal quarter ended March 31, 2019, filed on May 14, 2019; for the fiscal quarter ended June 30, 2019, filed on August 15, 2019; and for the fiscal quarter ended September 30, 2019, filed on November 14, 2019 (including Amendment No. 1 to Quarterly Report on Form 10-Q filed on November 14, 2019); |

| ● | Current Reports on Form 8-K filed on January 4, 2019, January 31, 2019, March 22, 2019, April 8, 2019, April 24, 2019, April 24, 2019, April 26, 2019, August 7, 2019, September 3, 2019, September 26, 2019, October 21, 2019, October 29, 2019, October 31, 2019, November 6, 2019, November 18, 2019 and December 12, 2019; and |

| ● | The description of our common stock contained in our Registration Statement on Form 8-A filed with the SEC on November 2, 2018, including any amendments or reports filed for the purpose of updating that description. |

You may request a copy of these filings, at no cost, by writing or telephoning us at the following address or phone number:

Avalon GloboCare Corp.

4400 Route 9 South

Suite 3100

Freehold, New Jersey 07728

Attention: Chief Financial Officer

732-780-4400

S-7

PROSPECTUS

$50,000,000

Common Stock

Preferred Stock

Warrants

Units

We may offer, from time to time, in one or more offerings, common stock, preferred stock, warrants or units, which we collectively refer to as the “securities”. The aggregate initial offering price of the securities that we may offer and sell under this prospectus will not exceed $50,000,000. We may offer and sell any combination of the securities described in this prospectus in different series, at times, in amounts, at prices and on terms to be determined at, or prior to, the time of each offering. This prospectus describes the general terms of these securities and the general manner in which these securities will be offered. We will provide the specific terms of these securities in supplements to this prospectus. The prospectus supplements will also describe the specific manner in which these securities will be offered and may also supplement, update or amend information contained in this prospectus. This prospectus may not be used to consummate a sale of securities unless accompanied by the applicable prospectus supplement. You should read this prospectus and any applicable prospectus supplement before you invest.

The securities covered by this prospectus may be offered through one or more underwriters, dealers and agents or directly to purchasers. The names of any underwriters, dealers or agents, if any, will be included in a supplement to this prospectus. For general information about the distribution of securities offered, please see “Plan of Distribution”.

Our common stock is listed on the Nasdaq Capital Market under the symbol “AVCO”. On January 11, 2019, the closing price of our common stock as reported by the Nasdaq Capital Market was $3.38 per share.

We completed a 1:4 reverse stock split of its common stock on October 18, 2016. All share and per share information has been retroactively adjusted to reflect this reverse stock split.

We are an “emerging growth company” as defined in section 3(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and are therefore eligible for certain exemptions from various reporting requirements applicable to reporting companies under the Exchange Act. (See “Exemptions Under the Jumpstart Our Business Startups Act.”)

Unless otherwise specified in an applicable prospectus supplement, our preferred stock, warrants and units will not be listed on any securities or stock exchange or on any automated dealer quotation system.

In reviewing this prospectus and the documents incorporated herein by reference you should carefully consider the matters described under the caption “Risk Factors”.

This investment involves a high degree of risk. You should purchase securities only if you can afford a complete loss.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this Prospectus is February 4, 2019

TABLE OF CONTENTS

i

This prospectus is a part of a registration statement that we have filed with the SEC utilizing a “shelf” registration process. Under this shelf registration process, we may sell any combination of the securities described in this prospectus in one or more offerings up to an aggregate offering price of $50,000,000.

Each time we sell securities, we will provide a supplement to this prospectus that contains specific information about the securities being offered and the specific terms of that offering. The supplement may also add, update or change information contained in this prospectus. If there is any inconsistency between the information in this prospectus and any prospectus supplement, you should rely on the prospectus supplement.

We may offer and sell securities to, or through, underwriting syndicates or dealers, through agents or directly to purchasers. The prospectus supplement for each offering of securities will describe in detail the plan of distribution for that offering.

In connection with any offering of securities (unless otherwise specified in a prospectus supplement), the underwriters or agents may over-allot or effect transactions which stabilize or maintain the market price of the securities offered at a higher level than that which might exist in the open market. Such transactions, if commenced, may be interrupted or discontinued at any time. See “Plan of Distribution.”

Please carefully read both this prospectus and any prospectus supplement together with the documents incorporated herein by reference under “Incorporation by Reference” and the additional information described below under “Where You Can Find More Information.”

Prospective investors should be aware that the acquisition of the securities described herein may have tax consequences. You should read the tax discussion contained in the applicable prospectus supplement and consult your tax advisor with respect to your own particular circumstances.

You should rely only on the information contained or incorporated by reference in this prospectus and any prospectus supplement. We have not authorized anyone to provide you with different information. The distribution or possession of this prospectus in or from certain jurisdictions may be restricted by law. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted or where the person making the offer or sale is not qualified to do so or to any person to whom it is not permitted to make such offer or sale. The information contained in this prospectus is accurate only as of the date of this prospectus and any information incorporated by reference is accurate as of the date of the applicable document incorporated by reference, regardless of the time of delivery of this prospectus or of any sale of the securities. Our business, financial condition, results of operations and prospects may have changed since those dates.

In this prospectus and in any prospectus supplement, unless the context otherwise requires, references to:

| ● | the term(s) “we”, “us”, “our”, “Company”, “our company”, “Avalon GloboCare” and “Avalon” refer to Avalon GloboCare Corp., a Delaware corporation, either alone or together with our consolidated subsidiaries as the context requires. |

| ● | “Exchange Act” refers to the Securities Exchange Act of 1934, as amended. |

| ● | “Securities Act” refers to the Securities Act of 1933, as amended. |

| ● | “FINRA” refers to the Financial Industry Regulatory Authority. |

| ● | “Nasdaq” refers to the Nasdaq Capital Market. |

| ● | “SEC” or the “Commission” refers to the United States Securities and Exchange Commission. |

| ● | “prospectus” includes this document and any information incorporated herein by reference. |

We completed a 1:4 reverse stock split of its common stock on October 18, 2016. All share and per share information has been retroactively adjusted to reflect this reverse stock split.

1

Overview

We are dedicated to integrating and managing global healthcare services and resources, as well as empowering high-impact biomedical innovations and technologies to accelerate their clinical applications. Operating through two major platforms, namely “Avalon Cell” and “Avalon Rehab”, our “Technology + Service” ecosystem covers the areas of regenerative medicine, cell-based immunotherapy, exosome technology, as well as rehabilitation medicine. We plan to integrate these services through joint ventures and accretive acquisitions that bring shareholder value both in the short term, through operational entities as part of Avalon Rehab, and long term, through biomedical innovation development as part of Avalon Cell, such as our recent joint venture for the advancement of exosome isolation systems and related products.

In addition, we are engaged in the development of exosome technology to improve the diagnosis and management of diseases. Exosomes are tiny, subcellular, membrane-bound vesicles 30-150 nm in diameter that are released by almost all cell types and can carry membrane and cellular proteins, as well as genetic materials that are representative of the cell of origin. Profiling various bio-molecules in exosomes may serve as useful biomarkers for a wide variety of diseases. Our isolation system is designed to be used by researchers for biomarker discovery and clinical diagnostic development, and advancement of targeted therapies. Currently, isolation systems and service are available to isolate exosomes or extract exosomal RNA/protein from serum/plasma, urine and saliva samples. We are seeking to decode proteomic and genomic alterations underlying a wide-range of pathologies, thus allowing for the introduction of novel non-invasive “liquid biopsies”. Our mission is focused on diagnostic advancements in the fields of oncology, infectious diseases and fibrotic diseases, and the discovery of disease-specific exosomes to provide the disease origin insight necessary to enable personalized clinical management. There is no guarantee that we will be able to successfully achieve our stated mission.

We currently generate revenue by selling exosome isolation systems in China and the United States through our joint venture GenExosome Technologies, Inc. In addition, we provide medical related consulting services in advanced areas of immunotherapy and second opinion/referral services through our wholly-owned subsidiary Avalon (Shanghai) Healthcare Technology Co., Ltd., or Avalon Shanghai. We also own and operate commercial real estate in New Jersey, where we are headquartered.

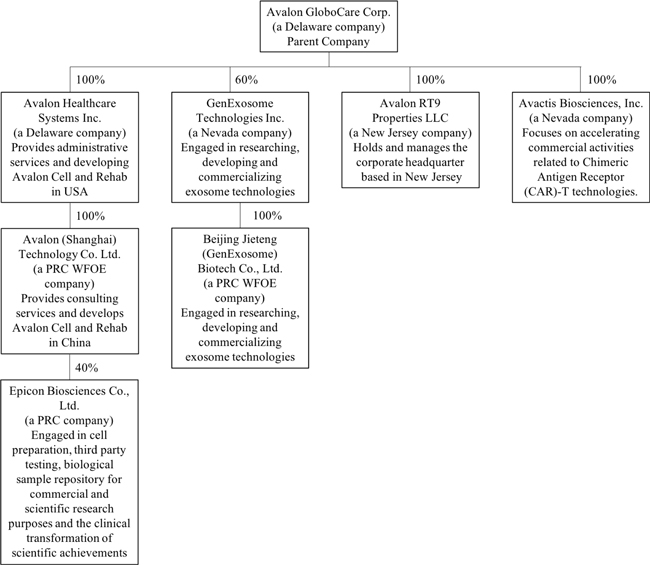

On May 29, 2018, Avalon Shanghai entered into a Joint Venture Agreement with Jiangsu Unicorn Biological Technology Co., Ltd., or Unicorn, pursuant to which a company named Epicon Biosciences Co., Ltd. (“Epicon”) was formed on August 14, 2018. Epicon is owned 60% by Unicorn and 40% by Avalon Shanghai. Within two years of execution of the Joint Venture Agreement, Unicorn shall invest cash into Epicon in an amount not less than RMB 8,000,000 (approximately $1.2 million) and the premises of the laboratories of Nanjing Hospital of Chinese Medicine for exclusive use by Epicon, and Avalon Shanghai shall invest cash into Epicon in an amount not less than RMB 10,000,000 (approximately $1.5 million). As of the date of this prospectus, Unicorn has invested the premises of the laboratories of Nanjing Hospital of Chinese Medicine and Avalon Shanghai has contributed RMB 3,000,000 (approximately $0.4 million). Epicon is focused on cell preparation, third party testing, biological sample repository for commercial and scientific research purposes and the clinical transformation of scientific achievements.

On July 18, 2018, we formed a wholly owned subsidiary, Avactis Biosciences, Inc., a Nevada corporation, which will be focused on accelerating commercial activities related to Chimeric Antigen Receptor (CAR)-T technologies. The subsidiary is designed to integrate and optimize our global scientific and clinical resources to further advance the use of CAR-T to treat certain cancers.

2

On July 30, 2018, we signed a Letter of Intent with Arbele Limited, a Hong Kong company (“Arbele”) for a proposed strategic partnership agreement. The purpose of the proposed transaction is to form a joint venture company, AVAR BioTherapeutics (China) Co. Ltd., to develop, manufacture, and commercializing CAR-T immunotherapy for treating cancer patients in China, utilizing intellectual property from Arbele and the clinical platform of the LuDaopei Medical Group in China. We paid a $100,000 fee to Arbele for a five-month exclusive right to complete the definitive agreements for the transaction.

On August 6, 2018, we entered into a strategic partnership agreement with Weill Cornell’s cGMP Cellular Therapy Facility and Laboratory for Advanced Cellular Engineering headed by Dr. Yen-Michael Hsu. This strategic partnership aims to co-develop bio-production and standardization procedures in procurement, storage, processing, clinical study protocols, and bio-banking for Chimeric Antigen Receptor (CAR)-T therapy, in accordance with the Foundation of Accreditation for Cellular Therapy (FACT) and American Association of Blood Banks (AABB) standards. This partnership also includes a CAR-T education program to support and foster collaborative research and training programs for scientists and clinicians between Weill Cornell and Hebei Yanda LuDaopei Hospital, which is our main affiliated clinical facility as well as the world’s single largest medical institution in CAR-T therapy.

On October 23, 2018, Avactis Biosciences, Inc. (“Avactis”) and Arbele Limited (“Arbele”) agreed to the establishment of AVAR BioTherapeutics (China) Co. Ltd. (“AVAR”), a Sino-foreign equity joint venture, pursuant to an Equity Joint Venture Agreement (the “AVAR Agreement”), which will be owned 60% by Avactis and 40% by Arbele. The purpose and business scope of the Joint Venture is to research, develop, produce, sell, distribute and generally commercialize CAR-T/CAR-NK/TCR-T/universal cellular immunotherapy in China. Avactis is required to contribute USD $10 million (or equivalent in RMB) in cash and/or services, which shall be contributed in tranches based on milestones to be determined jointly by AVAR and Avactis in writing subject to Avactis’ cash reserves. Within 30 days, Arbele shall make contribution of USD $6.66 million in the form of entering into a License Agreement with AVAR granting AVAR with an exclusive right and license in China to its technology and intellectual property pertaining to CAR-T/CAR-NK/TCR-T/universal cellular immunotherapy technology and any additional technology developed in the future with terms and conditions to be mutually agreed upon Avactis and AVAR and services. As of the date of this prospectus, AVAR is in process of being established and the License Agreement has not been finalized.

Corporate Information

We were incorporated under the laws of the State of Delaware on July 28, 2014 under the name Global Technologies Corp. On October 18, 2016, we changed our name to Avalon GloboCare Corp. and completed a reverse split of our shares of common stock at a ratio of 1:4.

We own 100% of the capital stock of Avalon Healthcare Systems, Inc., a Delaware corporation, or AHS, which we acquired on October 19, 2016. AHS was incorporated on May 18, 2015 under the laws of the State of Delaware. In addition, we own through AHS 100% of the capital stock of Avalon (Shanghai) Healthcare Technology Co., Ltd., or Avalon Shanghai, which is a wholly foreign-owned enterprise, or WOFE, organized under the laws of the People’s Republic of China, or PRC or China. Avalon Shanghai was incorporated on April 29, 2016 and is engaged in medical related consulting services for customers. On January 23, 2017, we incorporated Avalon (BVI) Ltd, a British Virgin Islands company (dormant and in process of being dissolved). On February 7, 2017, we formed Avalon RT 9 Properties, LLC, a New Jersey limited liability company. In July 2017, we formed GenExosome Technologies Inc., a Nevada corporation, or GenExosome. On October 25, 2017, we and GenExosome entered into a Securities Purchase Agreement pursuant to which we acquired 600 shares of GenExosome in consideration of $1,326,087 in cash and 500,000 shares of our common stock. On October 25, 2017, GenExosome entered into and closed an Asset Purchase Agreement with Yu Zhou, MD, PhD, pursuant to which we acquired all assets, including all intellectual property, held by Dr. Zhou pertaining to the business of researching, developing and commercializing exosome technologies in consideration of $876,087 in cash, 500,000 shares of our common stock and 400 shares of common stock of GenExosome. As a result of the above transactions, we hold 60% of GenExosome and Dr. Zhou holds 40% of GenExosome. On October 25, 2017, GenExosome entered into and closed a Stock Purchase Agreement with Beijing Jieteng (GenExosome) Biotech Co. Ltd., a corporation incorporated in the People’s Republic of China, Beijing GenExosome, and Dr. Zhou, the sole shareholder of Beijing GenExosome, pursuant to which GenExosome acquired all of the issued and outstanding securities of Beijing GenExosome in consideration of a cash payment in the amount of $450,000.

3

On July 18, 2018, we formed a wholly owned subsidiary, Avactis Biosciences Inc. (“Avactis”), a Nevada corporation, which will be focused on accelerating commercial activities related to cellular therapies, including regenerative medicine with stem/progenitor cells as well as cellular immunotherapy including CAR-T, CAR-NK, TCR-T and others. The subsidiary is designed to integrate and optimize our global scientific and clinical resources to further advance the use of cellular therapies to treat certain cancers. On October 23, 2018, Avactis and Arbele Limited (“Arbele”) agreed to the establishment of AVAR BioTherapeutics (China) Co. Ltd. (“AVAR”), a Sino-foreign equity joint venture, pursuant to an Equity Joint Venture Agreement (the “AVAR Agreement”), which will be owned 60% by Avactis and 40% by Arbele. The purpose and business scope of the Joint Venture is to research, develop, produce, sell, distribute and generally commercialize CAR-T/CAR-NK/TCR-T/universal cellular immunotherapy in China. Avactis is required to contribute USD $10 million (or equivalent in RMB) in cash and/or services, which shall be contributed in tranches based on milestones to be determined jointly by AVAR and Avactis in writing subject to Avactis’ cash reserves. Within 30 days, Arbele shall make contribution of USD $6.66 million in the form of entering into a License Agreement with AVAR granting AVAR with an exclusive right and license in China to its technology and intellectual property pertaining to CAR-T/CAR-NK/TCR-T/universal cellular immunotherapy technology and any additional technology developed in the future with terms and conditions to be mutually agreed upon Avactis and AVAR and services. As of the date of this prospectus, AVAR is in process of being established and the License Agreement has not been finalized.

The following diagram illustrates our corporate structure as of the date of this prospectus:

Sales and Marketing

We seek to develop new business through relationships driven by our senior management, which have extensive contacts throughout the healthcare system. Our senior management will be seeking opportunities for joint ventures, strategic relationships and acquisitions in consulting, biomedical innovations, and telemedicine, and rehabilitation centers.

4

Services

We currently generate revenue from related party strategic relationships through Avalon Shanghai that provide consultative services in advanced areas of immunotherapy and second opinion/referral services. In addition, our services are targeted at serving our clients and using our insights and deep expertise to produce tangible and significant results. Our services include research studies, executive education, daily online executive briefings, tailored expert advisory services, and consulting and management services. We typically charge an annual fee. Through our services, we attempt to have our clients focus on important problems by providing an analysis of the evolving healthcare industry and the methods prevalent in the industry to solve those problems through counsel, business planning and support. We tailor these solutions to the client’s specific strategic challenges, operational issues, and management concerns. We plan to expand our business services throughout the United States via our two major “Technology + Service” platforms: “Avalon Cell” and “Avalon Rehab”.

Strategic Partnerships

We are actively seeking potential strategic partnerships in our area of focus. In addition, we are actively seeking target acquisitions that add accretive value to our strategic plan. There is no guarantee that we will be able to successfully sign a definitive agreement, close or implement such business arrangement. Through our recent joint venture in the area of exosome technology, we are actively developing strategic relationships for the distribution and sale of our exosome isolation system and for the commercialization of exosome related products and diagnostic services.

Markets

We will focus on the following markets in developing our core business:

Platform “Avalon Cell”

Regarded as the future of medicine, we believe cell-based therapeutics will replace pharmaceuticals as a more effective and functional modality in disease treatment. We are actively engaging in this revolutionary trend and positioning to take a leading role in cell-based technology and therapeutics. The business model for our “Avalon Cell” platform is based on stringent criteria in the selection and evaluation of candidate projects at different stages of their developmental cycle. We particularly focus on projects that have strong intellectual property and distinctive innovation, as well as being translational, application-driven, and commercialization-ready. Our technology-based platform, “Avalon Cell”, comprises four programs:

| ● | Exosome technology, small extracellular vesicles that have great potential to be used as a vehicle for drug delivery in the treatment of various diseases and biomarkers for early stage diagnosis. We have commenced developing collaborative sites at Weill Cornell Medical College, MD Anderson Cancer Center and Mayo Clinic in the United States, as well as Lu Daopei Hospital of Daopei Medical Group and Da An Gene Co, Ltd., in China, focusing on exosome-based diagnostics, therapeutics, bio-banking, as well as “Exosomics Big Data”, in the unmet areas of oral cancer, ovary cancer and liver fibrosis; |

| ● | Endothelial cells, namely therapeutics involving the cells that line blood vessels and regulate exchanges between the bloodstream and surrounding tissue. These programs will occur with our collaborative sites at Weill Cornell Medical College Department of Pathology and Ansary Stem Cell Institute, focusing on standardization of endothelial cell banking and therapeutics; |

| ● | Regenerative medicine; and |

| ● | Cell-based immunotherapy (including cells such as NK, DC-CIK, CAR-T). |

5

Platform “Avalon Rehab”

A growing trend in China is in the sector of rehabilitation medicine. With our strong capabilities in integrating global technology and resources in physical medicine and rehabilitation, we will work towards positioning ourselves to take a leading role in this area through our “Avalon Rehab” platform. Our goal with this platform is to provide a turnkey, full suite of rehab services including physical therapy, occupational therapy, robotic engineering, cybernetics, and clinical nutrition. We will also engage in strategic partnerships with our institutional clients, building the leading and most authoritative network of integrated physical medicine and rehabilitation, particularly for cancer rehab patients. The focus will be on accretive acquisitions and joint venture strategic partnerships that are in revenue generating, cash flow positive positions to support biomedical innovation development while providing immediate shareholder value.

Revenue

GenExosome Technologies, Inc.

Through our majority-owned subsidiary, GenExosome Technologies, Inc., or GenExosome, we market and sell our proprietary exosome isolation systems. Exosomes are small extracellular vesicles that we believe may be used as a vehicle for drug delivery in the treatment of various diseases, and biomarkers for early stage diagnosis and as enhancements to certain cosmetic treatments and procedures. We currently produce our isolation systems in China and the U.S. and sell these systems primarily to research laboratories and universities.

Further, we generate revenue by performing development services for hospitals and sales of related products developed to hospitals through GenExosome and Beijing Jieteng (GenExosome) Biotech Co., Ltd., or Beijing GenExosome, GenExosome’s wholly-owned subsidiary.

Avalon RT 9 Properties, LLC

In May 2017, we acquired commercial property located in Freehold, New Jersey. This property is now our corporate headquarters and contains several commercial tenants that generate revenue through rental income. The revenue generated from the commercial tenants in our Freehold, New Jersey headquarters is facilitated through a management agreement with a company, which is controlled by Wenzhao Lu, our major shareholder and chairman of the Board of Directors, based in the United States.

Avalon Shanghai

We currently generate revenue by providing medical related consulting services in advanced areas of immunotherapy and second opinion/referral services through Avalon (Shanghai) Healthcare Technology Co., Ltd., or Avalon Shanghai. Our medical related consulting services include research studies, executive education, daily online executive briefings, tailored expert advisory services, and consulting and management services. Through our services we attempt to have our clients focus on important problems by providing an analysis of the evolving healthcare industry and the methods prevalent in the industry to solve those problems through counsel, business planning and support. The revenue generated from our related parties in China is managed by our employees residing in China and contactors who are retained as needed. Our contracts with the Ludaopei Hematology Research Institute Co., Ltd, a subsidiary of the Daopei Hospital Group (a related party of ours), expired as of March 31, 2018. On April 1, 2018, Avalon Shanghai entered into an advisory service contract with Beijing Ludaopei Blood Disease Research Institute Co., Ltd., a subsidiary of the Daopei Hospital Group (a related party of ours). Under the terms of the contract, the aggregate amount of advisory service fees was $300,000, which was invoiced by the end of 2018. The contract expired on December 31, 2018. Consulting services have been provided by Avalon Shanghai under the contract include:

| ● | providing scientific research consulting services; |

| ● | integrating experts, medical institutions and other resources in the United States in support of scientific research; |

6

| ● | providing technical education and training; and |

| ● | assisting in publication of academic papers. |

Strategic Development

We intend to focus on three components. The initial component will be focused on acquiring and/or managing fixed assets including healthcare real estate as well as stem cell banks. In addition, we intend to pursue the acquisition and development of healthcare related technologies for cell related diagnostics and therapeutics through acquisition, licensing or joint ventures with major universities and biotech companies. We will also consider a third avenue of investing in certain technologies for cell related diagnostics and therapeutics.

Intellectual Property

Our goal is to obtain, maintain and enforce patent rights for our products, formulations, processes, methods of use and other proprietary technologies, preserve our trade secrets, and operate without infringing on the proprietary rights of other parties, both in the United States and abroad. Our policy is to actively seek to obtain, where appropriate, the broadest intellectual property protection possible for our current product candidates and any future product candidates, proprietary information and proprietary technology through a combination of contractual arrangements and patents, both in the United States and abroad. Even patent protection, however, may not always afford us with complete protection against competitors who seek to circumvent our patents. If we fail to adequately protect or enforce our intellectual property rights or secure rights to patents of others, the value of our intellectual property rights would diminish. To this end, we require all of our employees, consultants, advisors and other contractors to enter into confidentiality agreements that prohibit the disclosure and use of confidential information and, where applicable, require disclosure and assignment to us of the ideas, developments, discoveries and inventions relevant to our technologies and important to our business.

Through GenExosome, we have applied for four patents in China with related trademarks. We are in the process of applying for those same patents and trademarks in the United States and are also in the process of developing additional patents and related intellectual property. We own and control a variety of trade secrets, confidential information, trademarks, trade names, copyrights, and other intellectual property rights that, in the aggregate, are of material importance to our business. We consider our trademarks, service marks, and other intellectual property to be proprietary, and rely on a combination of copyright, trademark, trade secret, non-disclosure, and contractual safeguards to protect our intellectual property rights.

Current patent applications in China are as follows.

| Application of an Exosomal MicroRNA in plasma as biomarker to diagnosis LIVER CANCER | Patent

application number: CN 2016 1 0675107.5 | |

| Clinical application of circulating exosome carried miRNA-33b in the diagnosis of liver cancer | Patent application

number: CN 2016 1 0675110.7 | |

| Saliva exosome-based methods and composition for the Diagnosis, Staging and Prognosis of ORAL CANCER | Patent application

number: CN 2017 1 0330847.X | |

| A novel exosome-based therapeutics against proliferative oral diseases | Patent application

number: CN 2017 1 0330835.7 |

Competition

GenExosome Technologies, Inc.

We currently market for sale our proprietary exosome isolation system. There are other companies that produce exosome isolation systems. However, our internal analysis shows that most exosome isolation systems use a centrifuge process for isolation which takes several hours and results in a low purity. Our isolation system is a membrane system which isolates exosomes in a few minutes with a higher purity than competing systems.

7

We believe that our proprietary isolation system is superior to competing systems and plan to continue to improve our process to maintain competitive advantages in the market.

Avalon Shanghai

In our current consulting business in the People’s Republic of China, or PRC or China, we compete with a number of advisory firm offering similar service including consulting and strategy firms; market research, data, benchmarking, and forecasting providers; technology vendors and services firms; healthcare information technology firms; technology advisory firms; outsourcing firms; and specialized providers of educational and training services. Other organizations, such as state and national trade associations, group purchasing organizations, non-profit think-tanks, and database companies, also may offer research, consulting, tools, and education services to health care and education organizations.

We believe that the principal competitive factors in our market include quality and timeliness of our services, strength and depth of relationships with our clients, ability to meet the changing needs of current and prospective clients, measurable returns on customer investment, and service and affordability.

As our business develops and we expand through joint ventures, acquisitions and strategic partnerships in the U.S. and PRC, we will have competition with other direct service providers, emerging technologies and medical communication platforms. We will seek to maintain a competitive advantage through intellectual property, superior quality management and cutting edge technology.

Rt. 9 Properties, LLC

Our executive commercial building in Freehold, New Jersey is located on a major highway and is one of the largest buildings in the surrounding areas. It is centrally located and maintains high occupancy. There are other commercial properties in the vicinity that offer similar amenities. However, premier executive offices are limited and as such we expect to continue to maintain high occupancy in the near term.

Manufacturing

GenExosome presently maintains its laboratory, research and manufacturing facilities in leased premises located in Beijing, China and Columbus, Ohio. We manufacture and assemble our exosome isolation systems for sale to research laboratories and universities. The exosome isolation system is comprised of our proprietary reagent with specifically designed membranes. We assemble the isolation system at our premises through commercially available purchased components that we modify in a proprietary manner and assemble in our systems, which are then shipped to our customers.

Legal Proceedings

From time to time, we are subject to ordinary routine litigation incidental to our normal business operations. We are not currently a party to, and our property is not subject to, any material legal proceedings.

Properties

Our principal offices are located at 4400 Route 9 South, Freehold, NJ 07728. The office building is owned by our subsidiary, Avalon RT 9 Properties, LLC, which is in business of owning and operating an income-producing real property. Our property is well maintained, adequately meets our needs, and is being utilized for its intended purpose.

We lease additional office space for operations. Office location is not crucial to our operations, and we anticipate no difficulty in extending these leases or obtaining comparable office space.

We are obligated under various lease agreements providing for office space that expire at various dates through the year 2019. Total rent expense under these lease agreements was $138,307 and $2,000 for the years ended December 31, 2017 and 2016, respectively.

8

We believe that our current office space is adequate for our current and immediately foreseeable operating needs.

Employees

As of December 20, 2018, we had 11 employees, nine of which are full time employees. Three full time employees and one part time employee are in the U.S. and six full time and one part time employees are in China. None of our employees are represented by a collective bargaining arrangement.

Government Regulation

Overview

The healthcare industry in the PRC and U.S. is highly regulated and subject to changing political, legislative, regulatory, and other influences. Further, the healthcare industry is currently undergoing rapid change. We are uncertain how, when or in what context these new changes will be adopted or implemented. These new regulations could create unexpected liabilities for us, could cause us or our members to incur additional costs and could restrict our or our clients’ operations. Many of the laws are complex and their application to us, our clients, or the specific services and relationships we have with our members are not always clear. Our failure to anticipate accurately the application of these laws and regulations, or our other failure to comply, could create liability for us, result in adverse publicity, and otherwise negatively affect our business.

Despite efforts to develop its legal system over the past several decades, including but not limited to legislation dealing with economic matters such as foreign investment, corporate organization and governance, commerce, taxation and trade, the PRC continues to lack a comprehensive system of laws. Further, the laws that do exist in the PRC are often vague, ambiguous and difficult to enforce, which could negatively affect our ability to do business in China and compete with other companies in our segments.

In September 2006, the Ministry of Commerce, or MOFCOM, promulgated the Regulations on Foreign Investors’ Mergers and Acquisitions of Domestic Enterprises, or the M&A Regulations, in an effort to better regulate foreign investment in the PRC. The M&A Regulations were adopted in part as a needed codification of certain joint venture formation and operating practices, and also in response to the government’s increasing concern about protecting domestic companies in perceived key industries and those associated with national security, as well as the outflow of well-known trademarks, including traditional Chinese brands.

As a U.S. based company doing business in the PRC, we seek to comply with all PRC laws, rules and regulations and pronouncements, and endeavor to obtain all necessary approvals from applicable PRC regulatory agencies such as the MOFCOM, the State Assets Supervision and Administration Commission, the State Administration for Taxation, the State Administration for Industry and Commerce, the China Securities Regulatory Commission, and the State Administration of Foreign Exchange, or SAFE.

Drug Approval Process